Chief Economist Eugenio J. Alemán discusses current economic conditions.

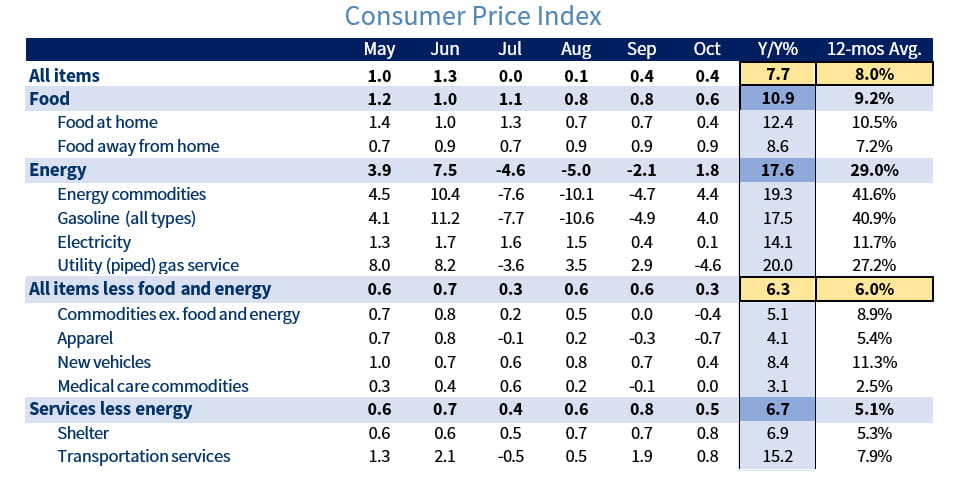

The market’s reaction to a better-than-expected inflation reading for October should not be a surprise, although the magnitude of the reaction looks a bit exaggerated. In our Weekly Economics of September 23, 2022, just after the September decision by the Federal Reserve (Fed), we said: “the Fed has put its worst-case scenario, something that should be music to the markets’ ears.” We further said: “For the markets, this should be good news even if it is very difficult to see it at this point. Since this is the worst- case scenario for the Fed, any ‘better-than-expected’ news in the inflation front should be a boon for markets.”

But markets should understand that this was just one month of data and that we had better-than-expected numbers before this latest October number and then we saw further deterioration, so markets should be cautious. Although we had very good news from several core goods and services sectors during the month of October, transportation services still managed to increase 0.8% during the month while the all-important shelter component of the index also increased 0.8% after increasing 0.7% in September. Thus, there are sectors of core prices that are still very strong. That is, if we don’t see weakness in the rest of the sectors, as we saw in October, then the probability of higher inflation readings remains. We do know that shelter prices are going to start to weaken in the next several quarters; but, while that train has departed the station, the wagons are going to take a relatively longer time to come through.

Furthermore, the higher oil and gasoline prices story is still not over. According to the latest Energy Information Administration (EIA) estimate, oil prices are expected to remain elevated during the rest of this year and into next year so the Fed is very aware that higher oil prices could, once again, threaten their efforts of bringing down inflation. Thus, the Fed is going to be very careful to keep interest rates high for a longer timeframe in order to buy time for shelter prices to start moving lower and building a buffer against higher oil prices in the future.

Alternative Scenarios:

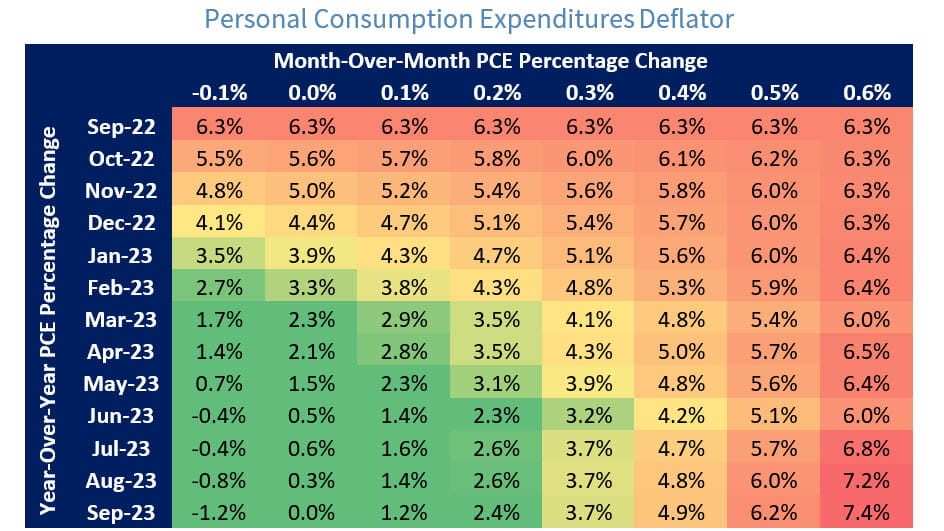

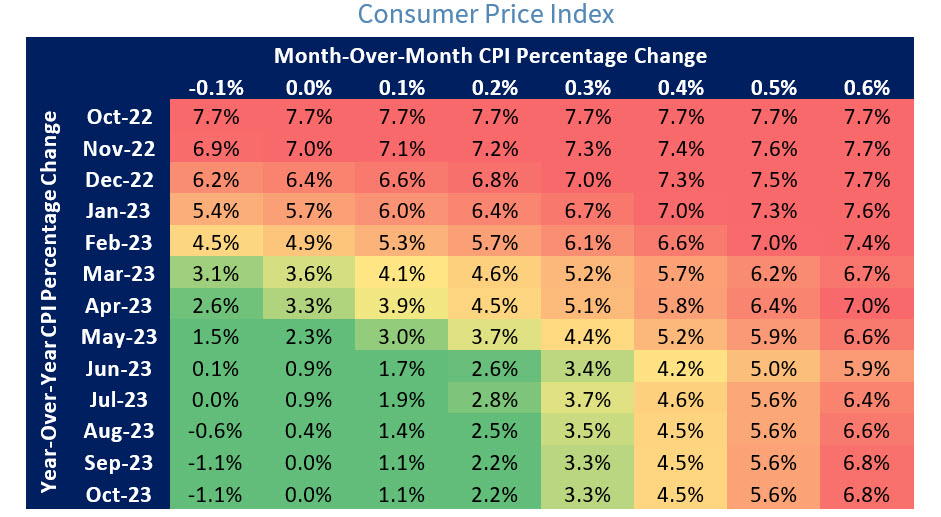

Below, we provide two tables of different scenarios for both, the PCE deflator and the CPI over the next year so we can see how inflation is going to evolve according to these scenarios. Of course, these scenarios assume that inflation will be the same for each month so it is an over simplification. However, it gives an idea of what monthly rates of inflation will allow the Fed to reach the 2.0% target for the PCE deflator.

The Federal Funds Rate, and the Neutral Federal Funds Rate

In a very interesting FRBSF (Federal Reserve Bank of San Francisco) Economic Letter entitled “Monetary Policy Stance is Tighter than Federal Funds Rate,” published on November 7, 2022, economists at the regional fed wrote a very insightful report on their view regarding the stance of monetary policy today. They calculated a proxy federal funds rate that includes “forward guidance as well as Quantitative Tightening (QT)” and concluded that “This proxy measure shows that, since late 2021, monetary policy has been substantially tighter than the federal funds rate indicates. Tightening financial conditions are similar to what would be expected if the funds rate had exceeded 5.25% by September 2022.”

However, the actual federal funds rate was at a range of 3.00% to 3.25% by September 2022, or more than 2 percentage points below this calculated “proxy” federal funds rate. This view of a proxy federal funds rate that is higher than the actual federal funds rate helps explain the surge in mortgage interest rates since the Federal Reserve (Fed) started its interest rate tightening campaign earlier this year and in some sense has accelerated the effects of monetary policy at least over the housing market.

At the same time, the argument of a tighter stance of monetary policy opens up the discussion of what is the level of what is normally called the “neutral federal funds rate,” which is the rate at which monetary policy is neither restrictive nor expansionary, that is, hurting or helping economic growth. Before the Covid-19 recession, the general view regarding the neutral federal funds rate was that it was close to 2.5%. However, over the years, the neutral federal funds rate has changed considerably. Back in 2012, the Federal Open Market Committee estimated a neutral rate of about 4.25% while during other periods, this rate has been at 3.5%.

For the Fed (and for economists trying to figure out the terminal rate during this tightening cycle), it is important to know what the Fed’s estimate for the current neutral rate is because this will determine where the Fed is ending its tightening campaign. The higher the neutral federal funds rate is, the higher their terminal federal funds rate will be.

Changes to Our Forecast

We have updated our economic forecast for 2023 and we have also extended the forecast to include 2024. The main feature of our new forecast is that we now have the recession starting during the second quarter of 2023 instead of the first quarter and lasting until the last quarter of the year. This change is predicated on the strength of the U.S. labor market and the staying power of the U.S. consumer, which has been able to navigate a higher inflation environment better than expected. However, this strength will weaken going forward.

We now have the U.S. economy flat in 2023 on an annual basis compared to our previous forecast of -0.5% for the year as a whole. Meanwhile, we have the economy growing by only 0.8% in 2023, which is below potential growth as we have inflation coming down but slower than in our previous forecast.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those Raymond James and are subject to change without notice the information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur last performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the U.S. Bureau of Labor Studies. Currencies investing are generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Consumer Sentiment is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in the first quarter of 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

Personal Consumption Expenditures Price Index (PCE): The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The change in the PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

Consumer confidence index is an economic indicator published by various organizations in several countries. In simple terms, increased consumer confidence indicates economic growth in which consumers are spending money, indicating higher consumption.

The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation.

Leading Economic Indicators: The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board's initial and ongoing certification requirements.

Currencies investing are generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

The STOXX Europe 600, also called STOXX 600, SXXP, is a stock index of European stocks designed by STOXX Ltd. This index has a fixed number of 600 components representing large, mid and small capitalization companies among 17 European countries, covering approximately 90% of the free-float market capitalization of the European stock market (not limited to the Eurozone).

Geographical Revenues: Overall country-specific revenues as a percentage of total revenues from a specific index such as the S&P 500 or the STOXX Europe 600.

Source: FactSet, data as of 9/30/2022